If you’ve ever wondered what accounting policies are, you’re not alone. Many people have a vague understanding of the term, but don’t really know what it encompasses. In this blog post, we’ll take a closer look at what accounting policies are and how they can impact your business.

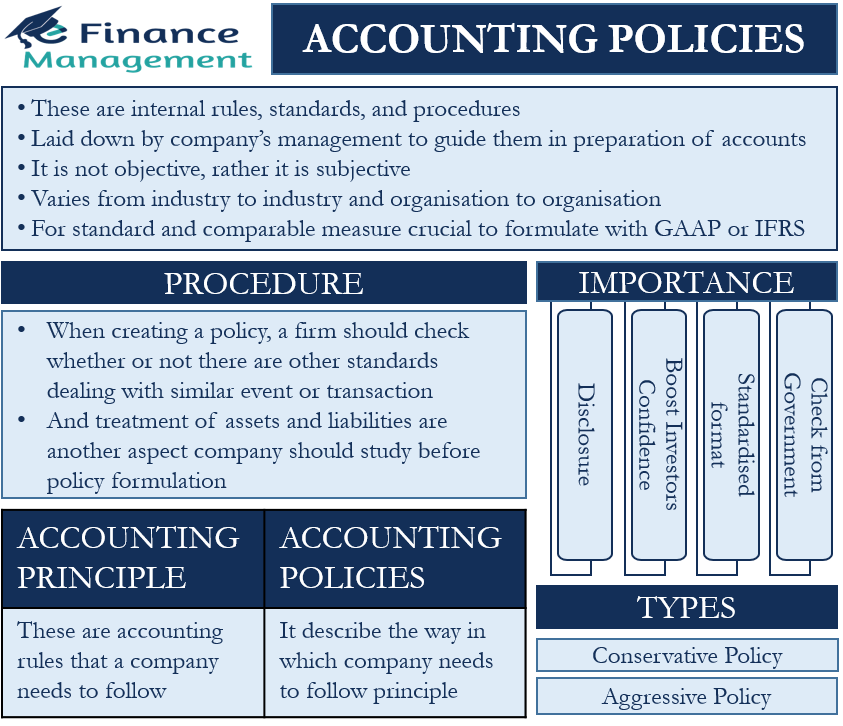

Accounting policies are the set of guidelines that a company follows when preparing financial statements. These guidelines can be specific to a certain country or region, or they may be set by the company itself. Either way, they should be followed consistently in order to produce accurate financial statements.

There are a few different types of accounting policies that companies may choose to follow. The most common include cash basis accounting, accrual basis accounting, and fair value accounting. Each of these has its own advantages and disadvantages, so it’s important to choose the one that’s right for your business.

Once you’ve selected the appropriate accounting policy for your business, you need to make sure that all of your financial statements are prepared in accordance with it. This includes your balance sheet, income statement, and cash flow statement. If any of these documents deviate from your chosen policy, it could cause confusion or even mislead your investors.

So

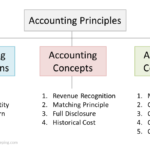

Accounting Policies Types

There are four types of accounting policies: mandatory, discretionary, accounting estimates, and disclosures.

1. Mandatory Accounting Policies: These are the policies that must be followed by all organizations, according to the Generally Accepted Accounting Principles (GAAP). An example of a mandatory policy would be the use of the accrual basis of accounting, which requires businesses to record revenue when it is earned and expenses when they are incurred, regardless of when cash is received or paid.

2. Discretionary Accounting Policies: These are policies that an organization has the choice to follow or not, as long as it is disclosed in the financial statements. An example of a discretionary policy would be the method used to depreciate assets.

3. Accounting Estimates: These are estimates that management makes about uncertain future events, such as the expected useful life of an asset or the amount of uncollectible accounts receivable. Since these estimates are based on assumptions, they may be revised in future periods as new information becomes available.

4. Disclosures: These are items that must be included in the financial statements in order for them to be complete and understandable. An example of a disclosure would be a description of the accounting methods used.

Financial Definition of Accounting Policies

The Accounting Policies financial definition of accounting policies refers to the specific guidelines that a company uses to account for its financial transactions. These policies can be either generally accepted accounting principles (GAAP) or internal accounting policies that are specific to the company.

Accounting policies are important because they provide guidance on how financial transactions should be recorded and reported. This is essential in ensuring that financial statements accurately reflect the company’s financial position and performance.

There are a number of different types of accounting policies that companies may use, depending on their specific needs. Some common accounting policy areas include revenue recognition, inventory valuation, and fixed asset depreciation.

It is important for companies to have well-defined accounting policies in place so that there is consistency in the way financial transactions are recorded and reported. This helps to ensure accuracy and comparability of financial statements over time.

Examples of Accounting Policies

There are a number of different accounting policies that businesses can adopt. Some common examples include:

-The way in which inventory is valued (e.g. using the first-in, first-out method or the last-in, first-out method)

-The method used to depreciate assets (e.g. straight-line depreciation or accelerated depreciation)

-The treatment of research and development costs (e.g. expensing all costs as they are incurred or capitalizing some costs)

Adopting specific accounting policies is a way for businesses to exercise judgement in financial reporting. The goal is to provide accurate and transparent financial information that conforms to generally accepted accounting principles (GAAP).

What Is Accounting Policies? – Accounting Policies Financial Definition

Accounting policies are the specific principles, rules, and procedures that a company uses to record and report its financial activities. These policies generally fall into three categories: financial reporting, asset valuation, and income tax.

A company’s accounting policies are typically detailed in its financial statements. For public companies, accounting policies are also disclosed in the footnotes to the financial statements.

When developing accounting policies, a company considers its business model, the industries it operates in, and its regulatory environment. The goal is to develop policies that accurately reflect the company’s financial position and performance.

There are many different types of accounting policies. Some common examples include:

– Revenue recognition: This policy dictates when and how revenue is recognized in the financial statements.

– Inventory valuation: This policy determines how inventory is valued on the balance sheet.

– Depreciation: This policy determines how assets are depreciated over time.

– Employee benefits: This policy determines how employee benefits (such as pensions and health insurance) are accounted for in the financial statements.