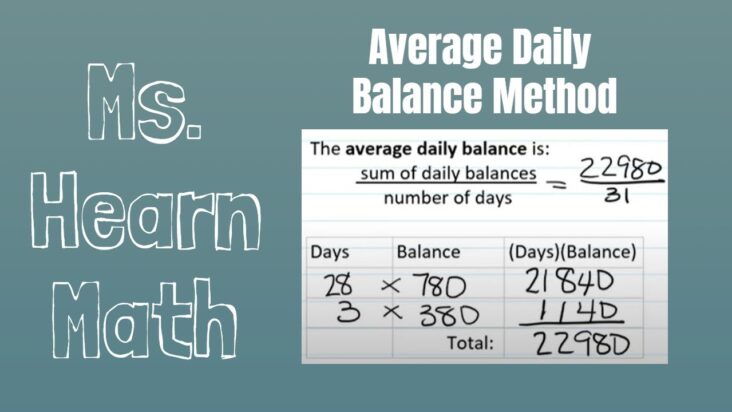

The Average Daily Balance Method is a common billing method used by creditors to calculate finance charges on credit cards. This method is designed to give customers a fair and accurate calculation of their monthly charges. By using the Average Daily Balance Method, creditors can ensure that a customer’s monthly payments are properly reflected in their finance charges. This article will explore how the Average Daily Balance Method works and how it can help customers better understand their monthly credit card payments.

What Is Average Daily Balance Method? – Average Daily Balance Method Financial Definition