An auditor’s opinion is an important tool for any business looking to assess their financial situation and identify potential risks. It is an assessment of the financial statements of a company and is provided by an external auditor. This opinion is vital for investors, creditors, and other stakeholders to gain insight into the financial health of a company. It is also used to help detect potential fraud and other financial irregularities. With an auditor’s opinion, a company is better prepared to make sound decisions and ensure they are in compliance with financial regulations.

Introduction to Auditor’s Opinion: Definition and Types

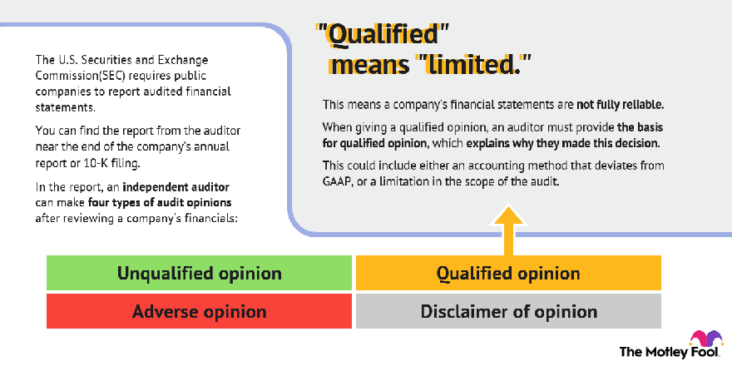

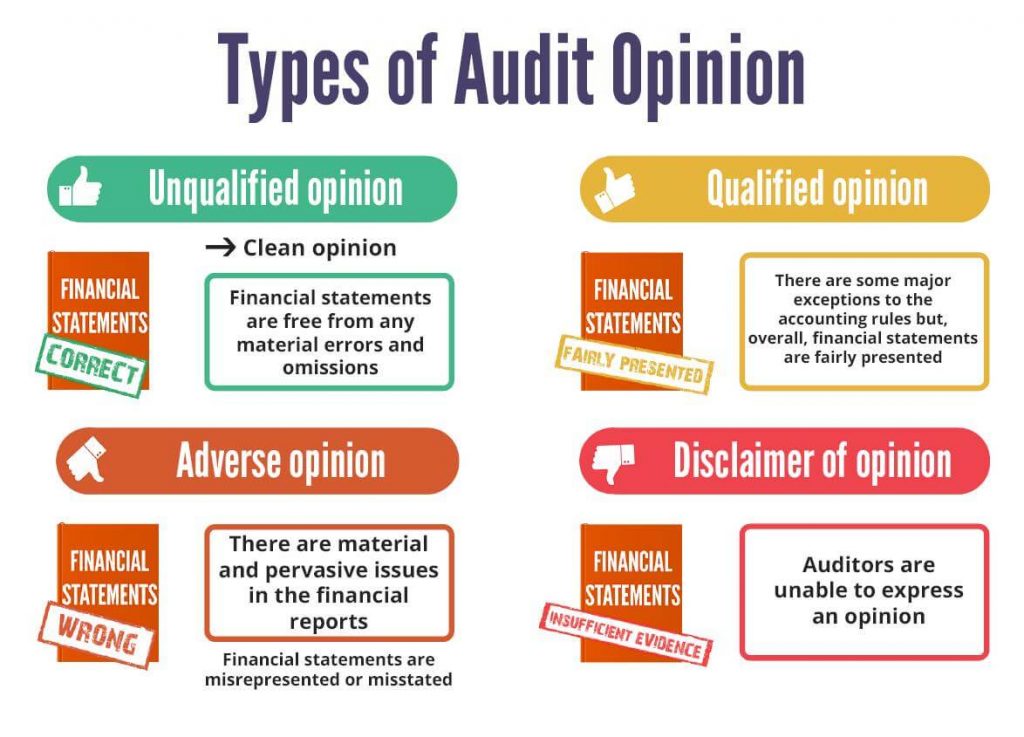

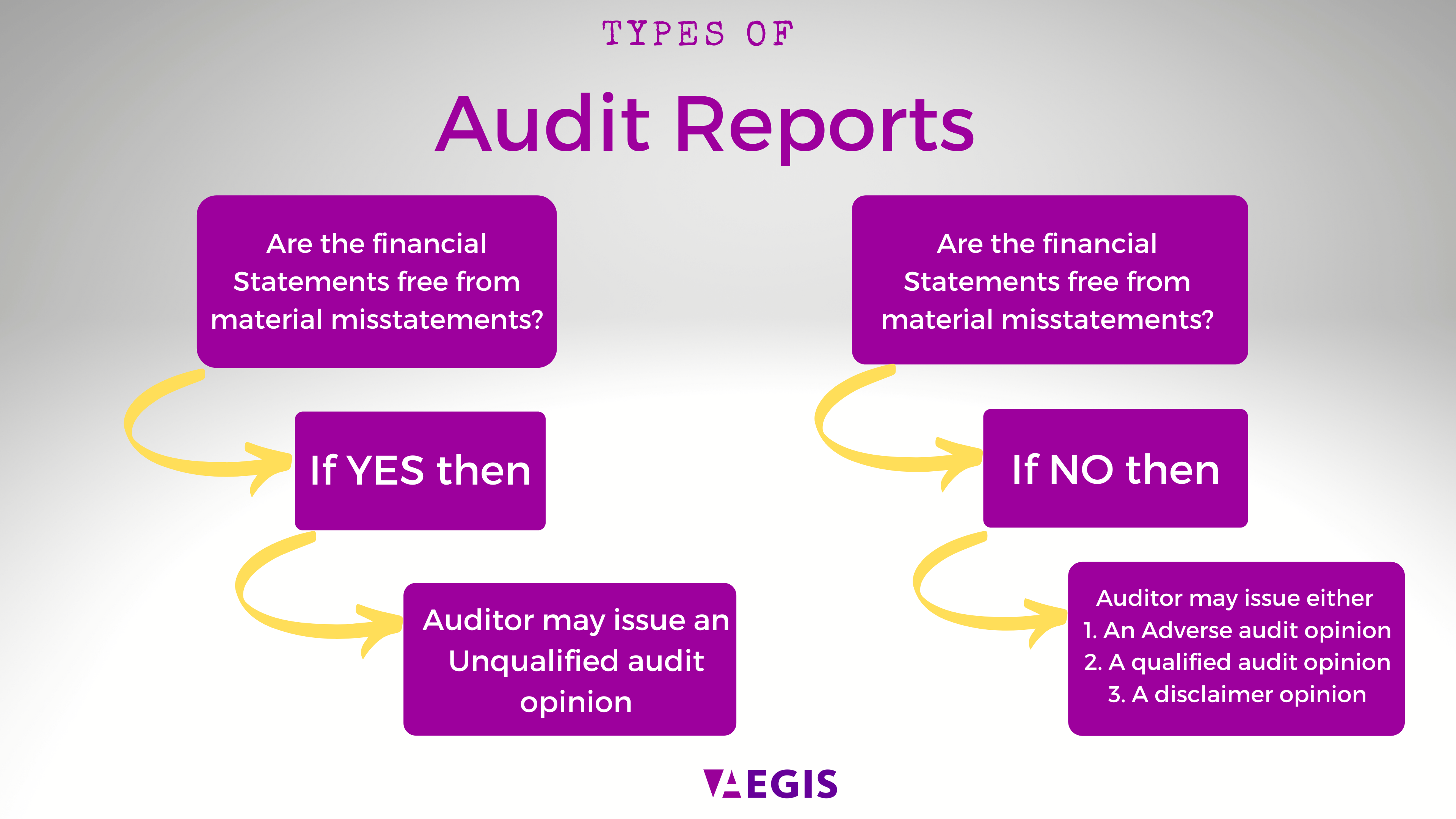

An auditor’s opinion is an important part of any financial statement. It confirms that the accounts have been examined by a professional, and that the financial statements are free from material misstatement. The auditor’s opinion is also known as an audit opinion. It is a professional opinion, formed after the auditor has examined the information and evidence available. An auditor’s opinion is typically expressed in the form of a letter accompanying the financial statements. There are three types of auditor’s opinion: unqualified, qualified and adverse. An unqualified opinion means that the financial statements are presented fairly, in all material respects. A qualified opinion means that the auditors had to make adjustments to the financial statements in order to present them fairly. An adverse opinion means that the financial statements do not present a fair picture. It is important to understand the auditor’s opinion before investing in a company. Knowing the opinion helps investors assess the financial stability of the company and make informed decisions.

Understanding the Different Types of Auditor’s Opinions

When it comes to understanding auditor’s opinions, it’s important to know that there are different types of opinions. Generally speaking, there are four types of auditor’s opinions that can be issued. The first type is a “clean” or “unqualified” opinion, which means that the auditor believes that the financial statements prepared by the company are accurate and reliable. The second type is a “qualified” opinion, which means that the auditor believes that there are some issues with the financial statements, but not enough to render them completely unreliable. The third type is an “adverse” opinion, which means that the auditor believes that the financial statements are unreliable and inaccurate. Finally, the fourth type is a “disclaimer” opinion, which means that the auditor is unable to form an opinion due to the lack of sufficient evidence. Understanding the different types of auditor’s opinions can help you make better decisions when dealing with financial statements.

Evaluating the Quality of an Auditor’s Opinion

An auditor’s opinion is one of the most important aspects of any financial report. An auditor’s opinion is the professional opinion of a CPA or other certified public accountant on the accuracy and reliability of the financial statements and other information presented in the report. It is important to thoroughly evaluate the quality of an auditor’s opinion when considering the financial report of a company. A qualified opinion is the best outcome of an audit, as it indicates that the auditor believes that the financial statements are free from material misstatements. An unqualified opinion, however, may still be a good sign if the auditor is able to provide an explanation as to why they are unable to give an opinion. The key to evaluating an auditor’s opinion is to understand the opinion and the reasoning behind it. When an auditor’s opinion is not satisfactory, it is important to consider the potential risks of relying on the financial statements.

Benefits of Having an Auditor’s Opinion

Having an Auditor’s Opinion is a must-have for any business. Not only does it provide assurance to potential investors, it also adds credibility and accountability to the financial statements of a company. An Auditor’s Opinion is a statement from an independent auditor that provides assurance on the accuracy of a company’s financial statements. This ensures that the financial statements are free from any material misstatement, and that the information presented is reliable. Furthermore, an Auditor’s Opinion can also provide protection for management and shareholders in the event of any potential claims or disputes. By having an independent auditor review financial statements, a company can gain the peace of mind that comes from knowing their financials are accurate and up to date. This can be invaluable in protecting the resources of the company, as well as providing assurance to potential investors that the company is prepared and reliable.

Potential Pitfalls to Avoid When Reading an Auditor’s Opinion

When reading an auditor’s opinion, it’s important to be aware of potential pitfalls that could lead to an inaccurate interpretation of the opinion. One of the most common problems is not distinguishing between an opinion on the financial statements, which is the auditor’s primary responsibility, and any other matters mentioned in the auditor’s report. For example, an auditor may provide an opinion on the company’s financial statements, but also include a separate opinion on the effectiveness of internal control over financial reporting. It’s important to read and understand the auditor’s opinion carefully, as it may include important details that could affect your interpretation of the financial statements. Additionally, you should be aware of any qualifications or disclaimers included in the opinion, as these can impact how the opinion should be interpreted. Finally, be sure to read any explanatory language included in the opinion, as this can provide additional insight into the auditor’s opinion. By familiarizing yourself with the potential pitfalls of reading an auditor’s opinion, you can ensure that you have a better understanding of what the opinion is actually saying.